Let  be an upper triangular matrix. The upper bounds for

be an upper triangular matrix. The upper bounds for  that we will discuss depend only on the absolute values of the elements of

that we will discuss depend only on the absolute values of the elements of  . This limits the ability of the bounds to distinguish between well-conditioned and ill-conditioned matrices. For example, consider

. This limits the ability of the bounds to distinguish between well-conditioned and ill-conditioned matrices. For example, consider

![\notag \begin{gathered} T_1 = \left[\begin{array}{crrrr} 1 & -2 & -2 & -2 & -2\\ & 1 & -2 & -2 & -2\\ & & 1 & -2 & -2\\ & & & 1 & -2\\ & & & & 1 \end{array}\right], \quad T_1^{-1} = \left[\begin{array}{ccccc} 1 & 2 & 6 & 18 & 54\\ & 1 & 2 & 6 & 18\\ & & 1 & 2 & 6\\ & & & 1 & 2\\ & & & & 1 \end{array}\right], \\ T_2 = \left[\begin{array}{ccccc} 1 & 2 & 2 & 2 & 2\\ & 1 & 2 & 2 & 2\\ & & 1 & 2 & 2\\ & & & 1 & 2\\ & & & & 1 \end{array}\right], \quad T_2^{-1} = \left[\begin{array}{crrrr} 1 & -2 & 2 & -2 & 2\\ & 1 & -2 & 2 & -2\\ & & 1 & -2 & 2\\ & & & 1 & -2\\ & & & & 1 \end{array}\right]. \end{gathered}](https://s0.wp.com/latex.php?latex=%5Cnotag+%5Cbegin%7Bgathered%7D++++++T_1+%3D+++++++%5Cleft%5B%5Cbegin%7Barray%7D%7Bcrrrr%7D+1+%26+-2+%26+-2+%26+-2+%26+-2%5C%5C+++++++++%26+1+%26+-2+%26+-2+%26+-2%5C%5C+++++++++%26+++%26+1+%26+-2+%26+-2%5C%5C+++++++++%26+++%26+++%26+1+%26+-2%5C%5C+++++++++%26+++%26+++%26+++%26+1+%5Cend%7Barray%7D%5Cright%5D%2C+%5Cquad++++++T_1%5E%7B-1%7D+%3D++++++%5Cleft%5B%5Cbegin%7Barray%7D%7Bccccc%7D++++++1+%26+2+%26+6+%26+18+%26+54%5C%5C++++++++%26+1+%26+2+%26+6+%26+18%5C%5C++++++++%26+++%26+1+%26+2+%26+6%5C%5C++++++++%26+++%26+++%26+1+%26+2%5C%5C++++++++%26+++%26+++%26+++%26+1++++++%5Cend%7Barray%7D%5Cright%5D%2C+%5C%5C+++++T_2+%3D+++++%5Cleft%5B%5Cbegin%7Barray%7D%7Bccccc%7D+++++1+%26+2+%26+2+%26+2+%26+2%5C%5C+++++++%26+1+%26+2+%26+2+%26+2%5C%5C+++++++%26+++%26+1+%26+2+%26+2%5C%5C+++++++%26+++%26+++%26+1+%26+2%5C%5C+++++++%26+++%26+++%26+++%26+1+++++%5Cend%7Barray%7D%5Cright%5D%2C+%5Cquad+++T_2%5E%7B-1%7D+%3D+++++%5Cleft%5B%5Cbegin%7Barray%7D%7Bcrrrr%7D++++++1+%26+-2+%26+2+%26+-2+%26+2%5C%5C++++++++%26+1+%26+-2+%26+2+%26+-2%5C%5C++++++++%26+++%26+1+%26+-2+%26+2%5C%5C++++++++%26+++%26+++%26+1+%26+-2%5C%5C++++++++%26+++%26+++%26+++%26+1+++++%5Cend%7Barray%7D%5Cright%5D.+%5Cend%7Bgathered%7D+&bg=ffffff&fg=222222&s=0&c=20201002)

The bounds for  and

and  will be the same, yet the inverses are of different sizes (the more so as the dimension increases).

will be the same, yet the inverses are of different sizes (the more so as the dimension increases).

Let  and write

and write

where  is strictly upper triangular and hence nilpotent with

is strictly upper triangular and hence nilpotent with  . Then

. Then

Taking absolute values and using the triangle inequality gives

where the inequalities hold elementwise.

The comparison matrix  associated with a general

associated with a general  is the matrix with

is the matrix with

It is not hard to see that  is upper triangular with

is upper triangular with  and so the bound (5) is

and so the bound (5) is

If we replace every element above the diagonal of by the most negative off-diagonal element in its row we obtain the upper triangular matrix  with

with

Then  , where

, where  , so

, so

Finally, let  , where

, where  is strictly upper triangular with every element above the diagonal equal to the maximum element of

is strictly upper triangular with every element above the diagonal equal to the maximum element of  , that is,

, that is,

Then

We note that , , and  are all nonsingular

are all nonsingular  -matrices. We summarize the bounds.

-matrices. We summarize the bounds.

Theorem 1.

If is a nonsingular upper triangular matrix then

We make two remarks.

- The bounds (6) are equally valid for lower triangular matrices as long as the maxima in the definitions of and are taken over columns instead of rows.

- We could equally well have written

. The comparison matrix

. The comparison matrix  is unchanged, and (6) continues to hold as long as the maxima in the definitions of and are taken over columns rather than rows.

is unchanged, and (6) continues to hold as long as the maxima in the definitions of and are taken over columns rather than rows.

It follows from the theorem that

for the 1-, 2-, and  -norms and the Frobenius norm. Now , , and all have nonnegative inverses, and for a matrix

-norms and the Frobenius norm. Now , , and all have nonnegative inverses, and for a matrix  with nonnegative inverse we have

with nonnegative inverse we have  . Hence

. Hence

where the big-Oh expressions show the asymptotic cost in flops of evaluating each term by solving the relevant triangular system. As the bounds become less expensive to compute they become weaker. The quantity  can be explicitly evaluated for

can be explicitly evaluated for  , using

, using  . It has the same value for

. It has the same value for  , and since

, and since  we have

we have

This bound is an equality for  for the matrix

for the matrix  in (1).

in (1).

For the Frobenius norm, evaluating  , and using

, and using  , gives

, gives

For the  -norm, either of (7) and (8) can be the smaller bound depending on

-norm, either of (7) and (8) can be the smaller bound depending on  .

.

For the special case of a bidiagonal matrix  it is easy to show that

it is easy to show that  , and so

, and so  can be computed exactly in

can be computed exactly in  flops.

flops.

These upper bounds can be arbitrarily weak, even for a fixed  , as shown by the example

, as shown by the example

for which

As  ,

,  . On the other hand, the overestimation is bounded as a function of for triangular matrices resulting from certain pivoting strategies.

. On the other hand, the overestimation is bounded as a function of for triangular matrices resulting from certain pivoting strategies.

Theorem 1.

Suppose the upper triangular matrix satisfies

Then, for the  -, -, and -norms,

-, -, and -norms,

Proof. The first four inequalities are a combination of (3) and (6). The fifth inequality is obtained from the expression (7) for  with

with  .

.

Condition (9) is satisfied for the triangular factors from QR factorization with column pivoting and for the transpose of the unit lower triangular factors from LU factorization with any form of pivoting.

The upper bounds we have described have been derived independently by several authors, as explained by Higham (2002).

![\notag \begin{bmatrix} a & x & 0 & 0 \\ & b & y & 0 \\ & & c & z \\ & & & d \end{bmatrix}^{-1} = \begin{bmatrix} \frac{1}{a} & -\frac{x}{a\,b} & \frac{x\,y}{a\,b\,c} & -\frac{x\,y\,z}{a\,b\,c\,d} \\[3pt] & \frac{1}{b} & -\frac{y}{b\,c} & \frac{y\,z}{b\,c\,d} \\[3pt] & & \frac{1}{c} & -\frac{z}{c\,d} \\[3pt] & & & \frac{1}{d} \end{bmatrix}.](https://s0.wp.com/latex.php?latex=%5Cnotag+%5Cbegin%7Bbmatrix%7D+a+++++++++++%26+x+++++++++++++++%26+0++++++++++++++++++++%26+0+%5C%5C+++++++++++++%26+b+++++++++++++++%26+y++++++++++++++++++++%26+0+%5C%5C+++++++++++++%26+++++++++++++++++%26+c++++++++++++++++++++%26+z+%5C%5C+++++++++++++%26+++++++++++++++++%26++++++++++++++++++++++%26+d+%5Cend%7Bbmatrix%7D%5E%7B-1%7D+%3D+%5Cbegin%7Bbmatrix%7D+%5Cfrac%7B1%7D%7Ba%7D+%26+-%5Cfrac%7Bx%7D%7Ba%5C%2Cb%7D+%26+%5Cfrac%7Bx%5C%2Cy%7D%7Ba%5C%2Cb%5C%2Cc%7D+%26+-%5Cfrac%7Bx%5C%2Cy%5C%2Cz%7D%7Ba%5C%2Cb%5C%2Cc%5C%2Cd%7D+%5C%5C%5B3pt%5D+++++++++++++%26+%5Cfrac%7B1%7D%7Bb%7D+++++%26+-%5Cfrac%7By%7D%7Bb%5C%2Cc%7D++++++%26+%5Cfrac%7By%5C%2Cz%7D%7Bb%5C%2Cc%5C%2Cd%7D++++++++%5C%5C%5B3pt%5D+++++++++++++%26+++++++++++++++++%26+%5Cfrac%7B1%7D%7Bc%7D++++++++++%26+-%5Cfrac%7Bz%7D%7Bc%5C%2Cd%7D+++++++++++++%5C%5C%5B3pt%5D+++++++++++++%26+++++++++++++++++%26++++++++++++++++++++++%26+%5Cfrac%7B1%7D%7Bd%7D+%5Cend%7Bbmatrix%7D.+&bg=ffffff&fg=222222&s=0&c=20201002)

depend on

, as there is no cancellation in the formulas for

(less obvious, and provable by a scaling argument).

![f[\dots]](https://s0.wp.com/latex.php?latex=f%5B%5Cdots%5D&bg=ffffff&fg=222222&s=0&c=20201002)

is upper bidiagonal then

is upper triangular with

and

![\notag f_{ij} = b_{i,i+1} b_{i+1,i+2} \dots b_{j-1,j}\, f[b_{ii},b_{i+1,i+1}, \dots, b_{jj}], \quad j > i.](https://s0.wp.com/latex.php?latex=%5Cnotag+++++++f_%7Bij%7D+%3D+b_%7Bi%2Ci%2B1%7D+b_%7Bi%2B1%2Ci%2B2%7D+%5Cdots+b_%7Bj-1%2Cj%7D%5C%2C++++++++++++++++f%5Bb_%7Bii%7D%2Cb_%7Bi%2B1%2Ci%2B1%7D%2C+%5Cdots%2C+b_%7Bjj%7D%5D%2C+%5Cquad+j+%3E+i.+&bg=ffffff&fg=222222&s=0&c=20201002)

of

of  , where

, where  is the matrix inverse. What is not always emphasized is that there are very few circumstances in which one should compute

is the matrix inverse. What is not always emphasized is that there are very few circumstances in which one should compute  ) system

) system  by computing

by computing  , but rather would carry out a division

, but rather would carry out a division  . In the

. In the  case, it is faster and more accurate to solve a linear system by LU factorization (Gaussian elimination) with partial pivoting than by inverting

case, it is faster and more accurate to solve a linear system by LU factorization (Gaussian elimination) with partial pivoting than by inverting  , where

, where  matrix with

matrix with  , satisfies the normal equations

, satisfies the normal equations  . It is therefore natural to form the symmetric positive definite matrix

. It is therefore natural to form the symmetric positive definite matrix  and solve the normal equations by Cholesky factorization. While fast, this method is numerically unstable when

and solve the normal equations by Cholesky factorization. While fast, this method is numerically unstable when

is the unit roundoff of the floating point arithmetic, then

is the unit roundoff of the floating point arithmetic, then

, in floating-point arithmetic

, in floating-point arithmetic  rounds to

rounds to

has been lost.

has been lost. , and in general the cost of the evaluation of a product depends on where one puts the parentheses. One order may be much superior to others, so one should not simply evaluate the product in a fixed left-right or right-left order. For example, if

, and in general the cost of the evaluation of a product depends on where one puts the parentheses. One order may be much superior to others, so one should not simply evaluate the product in a fixed left-right or right-left order. For example, if  ,

,  , and

, and  are

are  can be evaluated as

can be evaluated as : a vector outer product followed by a matrix–vector product, costing

: a vector outer product followed by a matrix–vector product, costing  : a vector scalar product followed by a vector scaling, costing just

: a vector scalar product followed by a vector scaling, costing just  in order to minimize the operation count is a

in order to minimize the operation count is a  ,

, for all

for all  ,

, factor is returned in the first argument, and it can be used to compute a direction of negative curvature (as needed in optimization), for example.

factor is returned in the first argument, and it can be used to compute a direction of negative curvature (as needed in optimization), for example.

that exploit the block structure and possible sparsity in

that exploit the block structure and possible sparsity in

in

in  operations, rather than the

operations, rather than the  operations required if the circulant structure is ignored.

operations required if the circulant structure is ignored. indicates a matrix that is nearly singular. However, the size of

indicates a matrix that is nearly singular. However, the size of  we can achieve any value for the determinant by multiplying by a scalar

we can achieve any value for the determinant by multiplying by a scalar  , yet

, yet  is no more or less nearly singular than

is no more or less nearly singular than  .

.

, yet

, yet

element of

element of  then the matrix becomes singular! By contrast,

then the matrix becomes singular! By contrast,  for all

for all  , where the

, where the  are the eigenvalue of

are the eigenvalue of  , it follows that the matrix condition number

, it follows that the matrix condition number  is bounded below by the ratio of largest to smallest eigenvalue in absolute value, that is,

is bounded below by the ratio of largest to smallest eigenvalue in absolute value, that is,

is a singular value decomposition (SVD), with

is a singular value decomposition (SVD), with  orthogonal and

orthogonal and  ,

,  . If

. If  and

and  are the same, but in general the eigenvalues

are the same, but in general the eigenvalues  can be very different.

can be very different.

, and future exascale computer systems will be able to tackle even larger problems. Rounding error analysis shows that the computed solution satisfies a componentwise backward error bound that, under favorable assumptions, is of order

, and future exascale computer systems will be able to tackle even larger problems. Rounding error analysis shows that the computed solution satisfies a componentwise backward error bound that, under favorable assumptions, is of order  , where

, where  for double precision and

for double precision and  for single precision. This backward error bound cannot guarantee any stability for single precision solution of today’s largest problems and suggests a loss of half the digits in the backward error for double precision.

for single precision. This backward error bound cannot guarantee any stability for single precision solution of today’s largest problems and suggests a loss of half the digits in the backward error for double precision. for both half precision formats, suggesting a potentially complete loss of numerical stability. Yet inner products with

for both half precision formats, suggesting a potentially complete loss of numerical stability. Yet inner products with  of two

of two

and

and  is the block size. The inner product has been broken into

is the block size. The inner product has been broken into  smaller inner products of size

smaller inner products of size  , which are computed independently then summed. Many linear algebra algorithms are blocked in an analogous way, where the blocking is into submatrices with

, which are computed independently then summed. Many linear algebra algorithms are blocked in an analogous way, where the blocking is into submatrices with  or

or  , so blocking brings a substantial reduction in the error bounds.

, so blocking brings a substantial reduction in the error bounds.

. By computing the sum

. By computing the sum  with a more accurate summation method the error constant is further reduced to

with a more accurate summation method the error constant is further reduced to  (this is the FABsum method of Blanchard et al. (2020)).

(this is the FABsum method of Blanchard et al. (2020)). rather than

rather than  for double precision, giving error bounds smaller by a factor up to

for double precision, giving error bounds smaller by a factor up to  .

. with one rounding error instead of two. This results in a reduction in error bounds by a factor

with one rounding error instead of two. This results in a reduction in error bounds by a factor  , with matrices

, with matrices  of fixed size, are available on Google tensor processing units, NVIDIA GPUs, and in the ARMv8-A architecture. For half precision inputs these devices can produce results of single precision quality, which can give a significant boost in accuracy when block FMAs are chained together to form a matrix product of arbitrary dimension.

of fixed size, are available on Google tensor processing units, NVIDIA GPUs, and in the ARMv8-A architecture. For half precision inputs these devices can produce results of single precision quality, which can give a significant boost in accuracy when block FMAs are chained together to form a matrix product of arbitrary dimension. when a corresponding worst-case bound is proportional to

when a corresponding worst-case bound is proportional to  , which is a significant reduction. Block FMAs and extended precision registers provide further reductions.

, which is a significant reduction. Block FMAs and extended precision registers provide further reductions. solved in single precision with a block size of

solved in single precision with a block size of  versus

versus  of a nonsingular matrix

of a nonsingular matrix  , for any matrix norm, where

, for any matrix norm, where  is the spectral radius (the largest magnitude of any eigenvalue of

is the spectral radius (the largest magnitude of any eigenvalue of

), but it can be arbitrarily weak for nonnormal matrices.

), but it can be arbitrarily weak for nonnormal matrices.

, where the

, where the  are of similar order of magnitude.

are of similar order of magnitude.

,

,  .

. matrices with

matrices with  , generated by

, generated by  the formula (3) is prone to overflow, which can be avoided by evaluating it in higher precision arithmetic.

the formula (3) is prone to overflow, which can be avoided by evaluating it in higher precision arithmetic.

,

,  of

of  . We can rewrite this upper bound as

. We can rewrite this upper bound as

larger than (4), this factor being attained for

larger than (4), this factor being attained for  .

. then (4) reduces to

then (4) reduces to

, where

, where  and

and  (thus

(thus  is a correlation matrix), using

is a correlation matrix), using

using (6). For example, for the

using (6). For example, for the  Pascal matrix

Pascal matrix![\notag P_5 = \left[\begin{array}{ccccc} 1 & 1 & 1 & 1 & 1\\ 1 & 2 & 3 & 4 & 5\\ 1 & 3 & 6 & 10 & 15\\ 1 & 4 & 10 & 20 & 35\\ 1 & 5 & 15 & 35 & 70 \end{array}\right]](https://s0.wp.com/latex.php?latex=%5Cnotag+P_5+%3D+%5Cleft%5B%5Cbegin%7Barray%7D%7Bccccc%7D+1+%26+1+%26+1+%26+1+%26+1%5C%5C+1+%26+2+%26+3+%26+4+%26+5%5C%5C+1+%26+3+%26+6+%26+10+%26+15%5C%5C+1+%26+4+%26+10+%26+20+%26+35%5C%5C+1+%26+5+%26+15+%26+35+%26+70+%5Cend%7Barray%7D%5Cright%5D+&bg=ffffff&fg=222222&s=0&c=20201002)

. The bounds from (4) and (5) are both

. The bounds from (4) and (5) are both  , whereas combining (4) and (7) gives a bound of

, whereas combining (4) and (7) gives a bound of  .

. for a matrix with integer entries. If a Cholesky, LU, or QR factorization of

for a matrix with integer entries. If a Cholesky, LU, or QR factorization of  is easily computable, but in this case a good order of magnitude estimate of the condition number can be cheaply computed using condition estimation techniques (Higham, 2002, Chapter 15).

is easily computable, but in this case a good order of magnitude estimate of the condition number can be cheaply computed using condition estimation techniques (Higham, 2002, Chapter 15). symmetric matrices with integer elements bounded by

symmetric matrices with integer elements bounded by  ; see

; see  is a factorization

is a factorization  , where

, where  and

and  are unitary and

are unitary and  , with

, with  , where where

, where where  . We sometimes write

. We sometimes write  to specify the matrix to which the singular value belongs.

to specify the matrix to which the singular value belongs. or

or  , whose eigenvalues are the squares of the singular values of

, whose eigenvalues are the squares of the singular values of

zero eigenvalues if

zero eigenvalues if  .

. ,

,

.

.

(the equality case in the Cauchy–Schwarz inequality). For example, (2) is equivalent to

(the equality case in the Cauchy–Schwarz inequality). For example, (2) is equivalent to

,

,

and nonsingular

and nonsingular  and

and  ,

,

.

.

. The bounds (5) and (6) are intuitively reasonable, because unitary transformations preserve singular values and the bounds quantify in different ways how close

. The bounds (5) and (6) are intuitively reasonable, because unitary transformations preserve singular values and the bounds quantify in different ways how close  and

and  are to being unitary.

are to being unitary. , and

, and  . Then

. Then

if

if  .

. is the leading principal submatrix of order

is the leading principal submatrix of order  ).

). and

and  . The first case is

. The first case is  , so that

, so that  and

and

, so

, so  and

and

. However, when

. However, when  may be less than the smallest singular value of

may be less than the smallest singular value of ![A = [A_{11}~A_{12}]](https://s0.wp.com/latex.php?latex=A+%3D+%5BA_%7B11%7D%7EA_%7B12%7D%5D&bg=ffffff&fg=222222&s=0&c=20201002) then

then  for all

for all  is easy to compute or estimate. Here, we focus on triangular matrices. The bounds we derive can be applied to a general matrix if an LU or QR factorization is available.

is easy to compute or estimate. Here, we focus on triangular matrices. The bounds we derive can be applied to a general matrix if an LU or QR factorization is available. any matrix norm, and we take the consistency condition

any matrix norm, and we take the consistency condition  as one of the defining properties of a matrix norm.

as one of the defining properties of a matrix norm.![\notag \left[\begin{array}{crrrr} 1 & -\theta & -\theta & -\theta & -\theta\\ & 1 & -\theta & -\theta & -\theta\\ & & 1 & -\theta & -\theta\\ & & & 1 & -\theta\\ & & & & 1 \end{array}\right]^{-1} = \left[\begin{array}{ccccc} 1 & \theta & \theta(1+\theta) & \theta(1+\theta)^2 & \theta(1+\theta)^3\\ & 1 & \theta & \theta(1+\theta) & \theta(1+\theta)^2\\ & & 1 & \theta & \theta(1+\theta)\\ & & & 1 & \theta\\ & & & & 1 \end{array}\right]](https://s0.wp.com/latex.php?latex=%5Cnotag+++++++%5Cleft%5B%5Cbegin%7Barray%7D%7Bcrrrr%7D+++++++1+%26+-%5Ctheta+%26+-%5Ctheta+%26+-%5Ctheta+%26+-%5Ctheta%5C%5C+++++++++%26+1+%26+-%5Ctheta+%26+-%5Ctheta+%26+-%5Ctheta%5C%5C+++++++++%26+++%26+1+%26+-%5Ctheta+%26+-%5Ctheta%5C%5C+++++++++%26+++%26+++%26+1+%26+-%5Ctheta%5C%5C+++++++++%26+++%26+++%26+++%26+1+%5Cend%7Barray%7D%5Cright%5D%5E%7B-1%7D+%3D++++++%5Cleft%5B%5Cbegin%7Barray%7D%7Bccccc%7D++++++1+%26+%5Ctheta+%26+%5Ctheta%281%2B%5Ctheta%29+%26+%5Ctheta%281%2B%5Ctheta%29%5E2+%26+%5Ctheta%281%2B%5Ctheta%29%5E3%5C%5C++++++++%26+1+%26+%5Ctheta+%26+%5Ctheta%281%2B%5Ctheta%29+%26+%5Ctheta%281%2B%5Ctheta%29%5E2%5C%5C++++++++%26+++%26+1+%26+%5Ctheta+%26+%5Ctheta%281%2B%5Ctheta%29%5C%5C++++++++%26+++%26+++%26+1+%26+%5Ctheta%5C%5C++++++++%26+++%26+++%26+++%26+1++++++%5Cend%7Barray%7D%5Cright%5D+&bg=ffffff&fg=222222&s=0&c=20201002)

be an eigenvalue with

be an eigenvalue with  (the spectral radius) and

(the spectral radius) and  , where

, where  is the vector of ones,

is the vector of ones,  , so

, so

since

since  . Hence

. Hence

, whose eigenvalues are its diagonal entries

, whose eigenvalues are its diagonal entries  , gives

, gives

gives

gives

, which yields another proof of (3) and (4).

, which yields another proof of (3) and (4). we have the lower bound

we have the lower bound  . We can choose

. We can choose  for

for  correct to within an order of magnitude.

correct to within an order of magnitude. by repeated triangular solves, obtaining the lower bound

by repeated triangular solves, obtaining the lower bound  . This bound is simply the power method applied to

. This bound is simply the power method applied to  .

. exceeds

exceeds  . Note that in some references, such as Horn and Johnson (2013), the reverse ordering is used, with

. Note that in some references, such as Horn and Johnson (2013), the reverse ordering is used, with  the largest eigenvalue. When it is necessary to specify what matrix

the largest eigenvalue. When it is necessary to specify what matrix  is an eigenvalue of we write

is an eigenvalue of we write  : the

: the  .

. is the quadratic form

is the quadratic form  for

for  . As

. As  , where

, where  is unitary and

is unitary and  . Then

. Then

, respectively, This characterization of the extremal eigenvalues of

, respectively, This characterization of the extremal eigenvalues of  is due to Lord Rayleigh (John William Strutt), and

is due to Lord Rayleigh (John William Strutt), and  is called a Rayleigh quotient. The intermediate eigenvalues correspond to saddle points of

is called a Rayleigh quotient. The intermediate eigenvalues correspond to saddle points of

are special cases of these characterizations.

are special cases of these characterizations. of Hermitian matrices. However, the Courant–Fischer theorem yields the upper and lower bounds

of Hermitian matrices. However, the Courant–Fischer theorem yields the upper and lower bounds

and

and  ,

,

. Inequality (3) with

. Inequality (3) with  gives

gives

, combined with (2), gives

, combined with (2), gives

to the interval between two adjacent eigenvalues of

to the interval between two adjacent eigenvalues of  , showing a possible configuration of the eigenvalues

, showing a possible configuration of the eigenvalues  of

of  A specific example, in MATLAB, is

A specific example, in MATLAB, is and the trace is the sum of the eigenvalues, we can write

and the trace is the sum of the eigenvalues, we can write

are nonnegative and sum to

are nonnegative and sum to  , the norm of the perturbation, then most of the increase in the eigenvalues is concentrated in the largest, since (5) bounds how much the smaller eigenvalues can change:

, the norm of the perturbation, then most of the increase in the eigenvalues is concentrated in the largest, since (5) bounds how much the smaller eigenvalues can change: positive eigenvalues and

positive eigenvalues and  negative eigenvalues then (3) with

negative eigenvalues then (3) with  gives

gives

gives

gives

eigenvalues appear in one of these inequalities and

eigenvalues appear in one of these inequalities and  appear in both. Therefore

appear in both. Therefore  of the eigenvalues are equal to

of the eigenvalues are equal to  eigenvalues can differ from

eigenvalues can differ from  changes at most

changes at most  and

and  and so taking

and so taking  in (3) and

in (3) and  in (4) gives

in (4) gives

.

.

interlace those of

interlace those of  for all

for all  interlace those of

interlace those of  is given in the next result.

is given in the next result.

in the formula

in the formula  that

that  for all

for all  . These relations are the first and last in a sequence of inequalities relating sums of eigenvalues to sums of diagonal elements obtained by Schur in 1923.

. These relations are the first and last in a sequence of inequalities relating sums of eigenvalues to sums of diagonal elements obtained by Schur in 1923.

is the set of diagonal elements of

is the set of diagonal elements of  .

.![[\lambda_1,\dots,\lambda_n]](https://s0.wp.com/latex.php?latex=%5B%5Clambda_1%2C%5Cdots%2C%5Clambda_n%5D&bg=ffffff&fg=222222&s=0&c=20201002) of eigenvalues majorizes the ordered vector

of eigenvalues majorizes the ordered vector ![[\widetilde{a}_{11},\dots,\widetilde{a}_{nn}]](https://s0.wp.com/latex.php?latex=%5B%5Cwidetilde%7Ba%7D_%7B11%7D%2C%5Cdots%2C%5Cwidetilde%7Ba%7D_%7Bnn%7D%5D&bg=ffffff&fg=222222&s=0&c=20201002) of diagonal elements.

of diagonal elements.

. Here is an illustration in MATLAB.

. Here is an illustration in MATLAB.

, the inequality is the same as the upper bound of (1), and for

, the inequality is the same as the upper bound of (1), and for  it is an equality:

it is an equality:  .

. is a congruence transformation. Sylvester’s law of inertia says that congruence transformations preserve the inertia. A result of Ostrowski (1959) goes further by providing bounds on the ratios of the eigenvalues of the original and transformed matrices.

is a congruence transformation. Sylvester’s law of inertia says that congruence transformations preserve the inertia. A result of Ostrowski (1959) goes further by providing bounds on the ratios of the eigenvalues of the original and transformed matrices. and

and

.

. and so Ostrowski’s theorem reduces to the fact that a congruence with a unitary matrix is a similarity transformation and so preserves eigenvalues. The theorem shows that the further

and so Ostrowski’s theorem reduces to the fact that a congruence with a unitary matrix is a similarity transformation and so preserves eigenvalues. The theorem shows that the further  is the maximum number of linearly independent columns, which is the dimension of the range space of

is the maximum number of linearly independent columns, which is the dimension of the range space of  . An important but non-obvious fact is that this is the same as the maximum number of linearly independent rows (see (5) below).

. An important but non-obvious fact is that this is the same as the maximum number of linearly independent rows (see (5) below). , where

, where  . A sum of

. A sum of

,

,  , …,

, …,  , so

, so  if

if  with

with

is the null space of

is the null space of

and applying the upper bound gives

and applying the upper bound gives  , and likewise with the roles of

, and likewise with the roles of

implies

implies  , and

, and  , which implies

, which implies  is defined,

is defined,

![B = [b_1,\dots,b_n]](https://s0.wp.com/latex.php?latex=B+%3D+%5Bb_1%2C%5Cdots%2Cb_n%5D&bg=ffffff&fg=222222&s=0&c=20201002) then

then ![AB = [Ab_1,\dots,Ab_n]](https://s0.wp.com/latex.php?latex=AB+%3D+%5BAb_1%2C%5Cdots%2CAb_n%5D&bg=ffffff&fg=222222&s=0&c=20201002) , so the columns of

, so the columns of  . Using (5) below, we then have

. Using (5) below, we then have

. Let the columns of

. Let the columns of  , so that

, so that  for some matrix

for some matrix  with

with  by the first part, so

by the first part, so  for some nonzero

for some nonzero  . But then

. But then  , which contradicts the linear independence of the columns of

, which contradicts the linear independence of the columns of  .

.

are both nonsingular

are both nonsingular  matrices by (2), so their product has rank

matrices by (2), so their product has rank

.

.

for nonsingular

for nonsingular  . Interchanging the roles of

. Interchanging the roles of  and so

and so

has rank

has rank  for some

for some  and

and  , both of rank

, both of rank  by (4). Conversely, suppose that

by (4). Conversely, suppose that  form a basis for the range space of

form a basis for the range space of  such that

such that  ,

,  , and with

, and with ![Y = [y_1,y_2,\dots, y_n]](https://s0.wp.com/latex.php?latex=Y+%3D+%5By_1%2Cy_2%2C%5Cdots%2C+y_n%5D&bg=ffffff&fg=222222&s=0&c=20201002) we have

we have  . Finally,

. Finally,  by (3), and since

by (3), and since  we have

we have  .

. submatrix.

submatrix. have some properties in common when both products are defined (notably they have the same nonzero eigenvalues),

have some properties in common when both products are defined (notably they have the same nonzero eigenvalues),  is not always equal to

is not always equal to  . A simple example is

. A simple example is  and

and  with

with  but

but  . An example with square

. An example with square

and

and  , where

, where  ) and are useful for constructing examples.

) and are useful for constructing examples.

and

and  are orthogonal,

are orthogonal,  . The rank of

. The rank of  with

with  , where

, where  is a constant and

is a constant and  . In general, we have no way to know whether tiny computed singular values signify exactly zero singular values. In practice, one typically defines a numerical rank based on a threshold and regards computed singular values less than the threshold as zero. Indeed the MATLAB

. In general, we have no way to know whether tiny computed singular values signify exactly zero singular values. In practice, one typically defines a numerical rank based on a threshold and regards computed singular values less than the threshold as zero. Indeed the MATLAB  , where

, where  is the largest computed singular value. If the data from which the matrix is constructed is uncertain then the definition of numerical rank should take into account the level of uncertainty in the data. Dealing with rank deficiency in the presence of data errors and in finite precision arithmetic is a tricky business.

is the largest computed singular value. If the data from which the matrix is constructed is uncertain then the definition of numerical rank should take into account the level of uncertainty in the data. Dealing with rank deficiency in the presence of data errors and in finite precision arithmetic is a tricky business. such that

such that

needs to make any negative eigenvalues of

needs to make any negative eigenvalues of  and assume that

and assume that  .

. ,

,  has eigenvalues

has eigenvalues  , and so the smallest possible

, and so the smallest possible  is

is  . This choice of

. This choice of  , so that each diagonal entry undergoes a relative perturbation of size

, so that each diagonal entry undergoes a relative perturbation of size  and note that

and note that  is symmetric with unit diagonal. Then

is symmetric with unit diagonal. Then

is positive semidefinite if and only if

is positive semidefinite if and only if  is positive semidefinite, the smallest possible

is positive semidefinite, the smallest possible  .

. as

as

(since

(since  and

and  .

. is positive semidefinite then from standard eigenvalue inequalities,

is positive semidefinite then from standard eigenvalue inequalities,

satisfies the constraints of

satisfies the constraints of  , this means that this

, this means that this  such that

such that  for an upper triangular

for an upper triangular  is positive definite. The methods of Gill, Murray, and Wright (1981) and Schnabel and Eskow (1990) compute a diagonal

is positive definite. The methods of Gill, Murray, and Wright (1981) and Schnabel and Eskow (1990) compute a diagonal  ) flops), so this approach is likely to require fewer flops than computing the minimum eigenvalue or solving an optimization problem, but the perturbations produces will not be optimal.

) flops), so this approach is likely to require fewer flops than computing the minimum eigenvalue or solving an optimization problem, but the perturbations produces will not be optimal. , so

, so  . The Gill–Murray–Wright method gives

. The Gill–Murray–Wright method gives  with diagonal elements

with diagonal elements while the Schnabel–Eskow method gives

while the Schnabel–Eskow method gives  with diagonal elements

with diagonal elements . If we increase the diagonal elements of

. If we increase the diagonal elements of  by 0.5 to give comparable smallest eigenvalues for the perturbed matrices then we have

by 0.5 to give comparable smallest eigenvalues for the perturbed matrices then we have

to be the matrix resulting from adding

to be the matrix resulting from adding  to the

to the  and

and  elements and we ask when is

elements and we ask when is

has rank

has rank  ,

,  repeated

repeated  times. Hence we can write

times. Hence we can write  , where

, where  and

and  . Adding

. Adding  to

to  decreases or leaves unchanged each eigenvalue. However, more is true: after each of these rank-

decreases or leaves unchanged each eigenvalue. However, more is true: after each of these rank- , we have (Horn and Johnson, Cor. 4.3.7)

, we have (Horn and Johnson, Cor. 4.3.7)

, so

, so  is the product of the eigenvalues of

is the product of the eigenvalues of  .

.

. Hence the condition for

. Hence the condition for

for

for

.

. is set to zero is

is set to zero is  , or equivalently

, or equivalently  . To check either of these conditions we need just

. To check either of these conditions we need just  ,

,  , and

, and  . These elements can be computed without computing the whole inverse by solving the equations

. These elements can be computed without computing the whole inverse by solving the equations  for

for  , for the

, for the  of

of  for

for  :

:![\notag A = \begin{bmatrix} 1 & \frac{1}{2} & \frac{1}{3} & \frac{1}{4} \\[3pt] \frac{1}{2} & 1 & \frac{2}{3} & \frac{1}{2} \\[3pt] \frac{1}{3} & \frac{2}{3} & 1 & \frac{3}{4} \\[3pt] \frac{1}{4} & \frac{1}{2} & \frac{3}{4} & 1 \end{bmatrix}.](https://s0.wp.com/latex.php?latex=%5Cnotag+++A+%3D+%5Cbegin%7Bbmatrix%7D+++++++++1+++++++++++%26+%5Cfrac%7B1%7D%7B2%7D++%26+%5Cfrac%7B1%7D%7B3%7D+%26+%5Cfrac%7B1%7D%7B4%7D+%5C%5C%5B3pt%5D+++++++++%5Cfrac%7B1%7D%7B2%7D+%26+++++++++++1++%26+%5Cfrac%7B2%7D%7B3%7D+%26+%5Cfrac%7B1%7D%7B2%7D+%5C%5C%5B3pt%5D+++++++++%5Cfrac%7B1%7D%7B3%7D+%26++%5Cfrac%7B2%7D%7B3%7D+%26+1+++++++++++%26+%5Cfrac%7B3%7D%7B4%7D+%5C%5C%5B3pt%5D+++++++++%5Cfrac%7B1%7D%7B4%7D+%26++%5Cfrac%7B1%7D%7B2%7D+%26+%5Cfrac%7B3%7D%7B4%7D+%26++1+++++++++%5Cend%7Bbmatrix%7D.+&bg=ffffff&fg=222222&s=0&c=20201002)

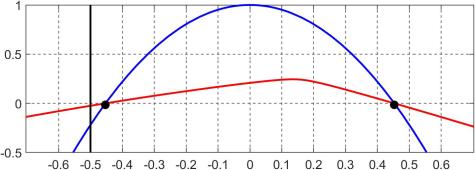

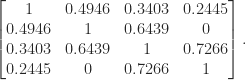

. Any off-diagonal element except the

. Any off-diagonal element except the  element can be zeroed without destroying positive definiteness, and if the

element can be zeroed without destroying positive definiteness, and if the  . For

. For  and

and  , the following plot shows in red

, the following plot shows in red  and in blue

and in blue  ; the black dots are the endpoints of the closure of the interval

; the black dots are the endpoints of the closure of the interval  and the vertical black line is the value

and the vertical black line is the value  . Clearly,

. Clearly,  , which is why zeroing this element causes a loss of positive definiteness. Note that

, which is why zeroing this element causes a loss of positive definiteness. Note that  to any number less than

to any number less than  without losing definiteness.

without losing definiteness.

of elements to be modified we may wish to determine subsets (including a maximal subset) of

of elements to be modified we may wish to determine subsets (including a maximal subset) of  on the smallest eigenvalue, which corresponds to another projection. Both these projections are supported in the algorithm of Higham and Strabić (2016), implemented in the code at

on the smallest eigenvalue, which corresponds to another projection. Both these projections are supported in the algorithm of Higham and Strabić (2016), implemented in the code at  is (to four significant figures)

is (to four significant figures)

-Factorizations with Small Pivots

-Factorizations with Small Pivots